Understanding the Medicare Premium and Deductible Changes for 2024

On October 12, 2023, the Centers for Medicare & Medicaid Services (CMS) unveiled significant Medicare updates for 2024. With shifts spanning across Medicare Parts A, B, and D, beneficiaries can expect adjustments in premiums, deductibles, and income-related monthly adjustments, as well as changes stemming from policies like the 340B-acquired drug payment policy. It's crucial to understand these updates to manage your Medicare coverage into 2024.

Medicare Part B in 2024

Medicare Part B, which covers physicians’ services, outpatient hospital care, and certain home health services, is seeing some financial adjustments. In 2024, the standard monthly premium will rise to $174.70 from $164.90 in 2023. Alongside this, the annual deductible—an initial amount you need to pay for your healthcare services before Medicare starts to chip in—will also increase to $240, up from $226.

These shifts are influenced by the projected growth in healthcare spending and adjustments related to the 340B-acquired drug payment policy, a program that allows certain hospitals and healthcare providers to purchase drugs at reduced prices. Changes in how these drugs are reimbursed can impact Medicare costs and, subsequently, premiums and deductibles.

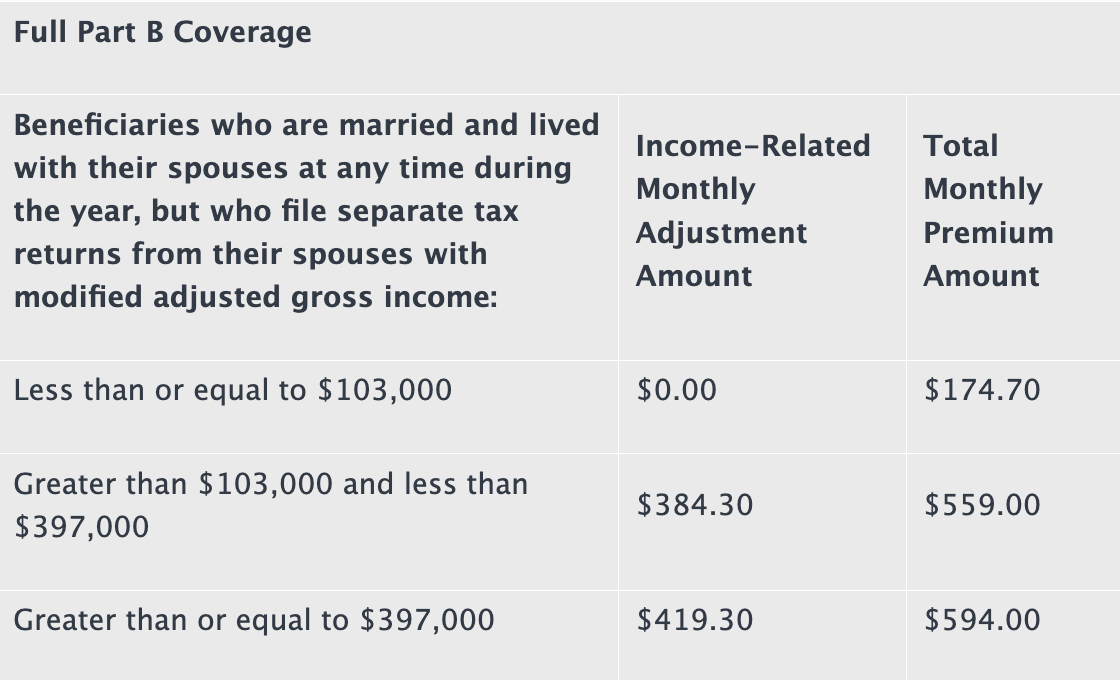

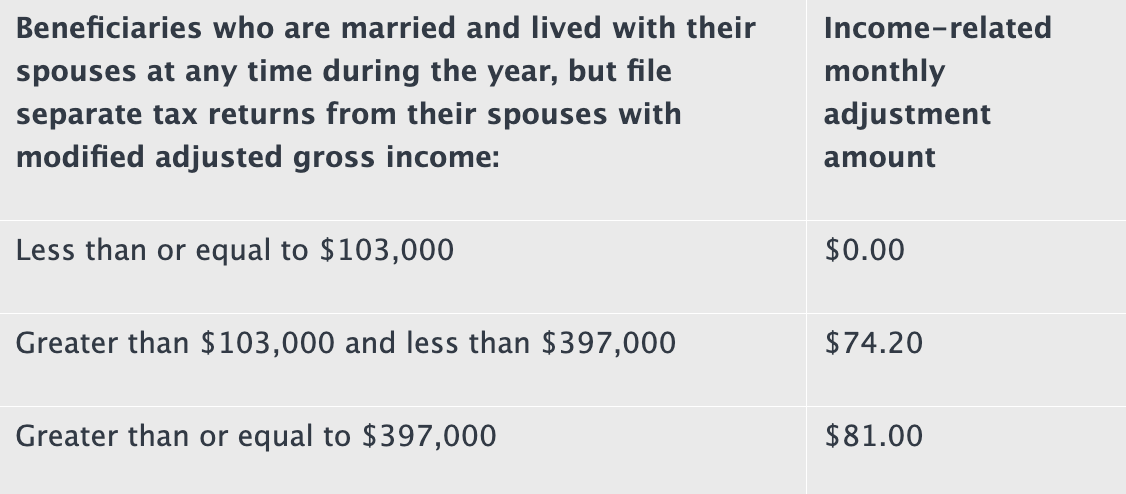

IRMAA in 2024

Medicare Part B's monthly premium has been tied to income since 2007 with the IRMAA (Income-Related Monthly Adjust Amount). For 2024, those in higher income brackets will experience premium adjustments. The specifics are detailed in the tables below, but it's essential to understand the different categories based on individually filed tax returns, jointly filed tax returns, and married but separately filed tax returns.

Additionally, there's a distinction between Full Part B Coverage and Part B Immunosuppressive Drug Coverage Only. The former refers to the standard coverage under Part B, while the latter is specific to those who only need coverage for immunosuppressive drugs, often after organ transplants.

To learn more check out our IRMAA in 2024 blog.

Source: cms.gov

Medicare Part A in 2024

Medicare Part A, which covers inpatient hospitals, skilled nursing facilities, and some home health care services, also has financial changes for 2024. The inpatient hospital deductible will rise to $1,632. After this deductible is met, beneficiaries will encounter coinsurance costs based on the length of their hospitalization.

Coinsurance is an additional portion of the cost of a service that you're responsible for paying. Medicare Part A coinsurance for 2024 is as follows:

For days 61 through 90 of a hospitalization, beneficiaries will have a coinsurance amount of $408 per day.

For lifetime reserve days (beyond the 90th day), the coinsurance will be $816 per day.

For beneficiaries in skilled nursing facilities, the daily coinsurance for days 21 through 100 of extended care services in a benefit period will be $204.

It's essential to note that the first 60 days of Medicare-covered inpatient hospital care in a benefit period are covered by the initial deductible and do not have a daily coinsurance amount.

Source: cms.gov

Medicare Part D in 2024

Medicare Part D, which covers for prescription drugs, has its own set of income-related adjustments. The tables below provide a comprehensive view of these adjustments, also based on income brackets.

To learn more check out our Part D in 2024 blog.

Source: cms.gov

A Commitment to Access and Affordability in 2024

Beyond the numbers, CMS's dedication to enhancing healthcare accessibility and affordability shines through. Initiatives like the Medicare Savings Programs (MSPs) and the Part D Low-Income Subsidy (LIS) have been instrumental in assisting beneficiaries. The recent introduction of the Inflation Reduction Act further expands the reach of these benefits. With these 2024 updates and clarifications, you're better equipped to navigate the Medicare landscape. If you're seeking personalized guidance, contact our licensed insurance agents today, at no additional cost.